Pension Annuities: Buy Now or Wait?

Since the pension freedoms introduced in April 2015, anyone aged 55 (Normal Minimum Pension Age (NMPA) will increase from 55 to 57 on 6 April 2028) or over with a defined contribution pension can take their pension as and how they wish, regardless of pot size. That flexibility is welcome, but it also makes deciding whether to convert your pension into an income a genuinely tricky decision.

Weighing up whether to buy now or wait? Call us free on 0800 098 7050 and we’ll talk you through your options.

Free 5-minute questionnaire | Whole of market search | No obligation

The Sting in the Tail of Taking Cash

Taking your money when you want it sounds appealing, doesn’t it? But it’s impossible to know what age you’ll live to, and tempting as it is to take the cash, there’s a catch: while you can usually take 25% as a tax-free lump sum, the remainder counts as earned income and is potentially taxable at a rate linked to all the income you receive that year.

If you need a secure, guaranteed income that lasts for the rest of your life, nothing about that has changed — an annuity is still the most suitable option for many people.

Gambling Your Future on Three Big Unknowns

You may still decide to delay buying an annuity — but this comes with its own risks. Delaying means gambling your future income on three things entirely outside your control:

- Annuity rates rise and fall. If they improve, you may get more income, but there’s no guarantee this will happen

- Your pension fund’s value fluctuates. If it increases while you’ve held off buying, you’ll have a larger fund that could buy a higher income — but the value could just as easily fall

- Your health may change. If it deteriorates, you could qualify for a higher Enhanced Annuity rate — but your health may simply remain the same

Let’s take a look at how these might actually play out.

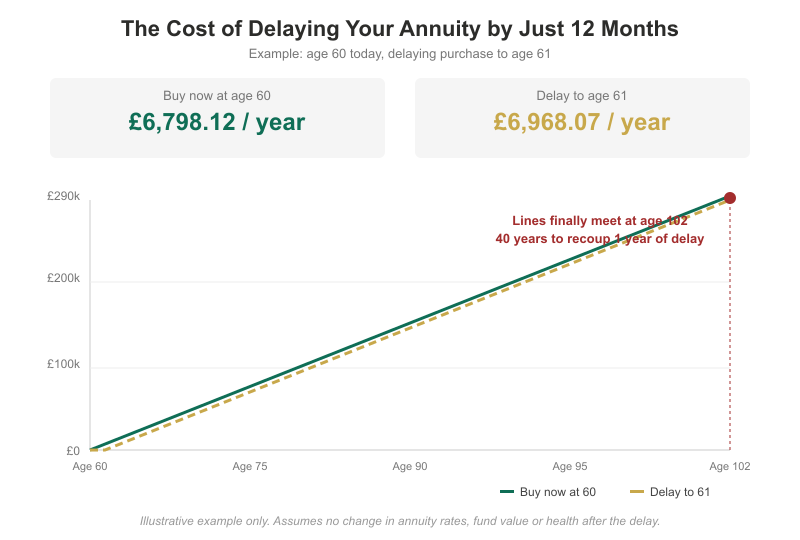

Cost of Delay — An Example

Based on an age of 60 today and a pension fund of £100,000 (please confirm this figure with us, as it determines the numbers below), and not taking any tax-free cash, you could receive an income of £6,798.12 annually.

Now let’s assume the annuity is delayed by 12 months, to age 61. You’ll receive a higher income because you’re a year older — which on the face of it sounds great. However, waiting until 61 means you’ll have missed out on a full year of payments: £6,798.12 in lost income. It could take many years to recoup what’s missed by delaying for just 12 months.

Assuming at age 61 that annuity rates haven’t increased, your pension fund hasn’t grown, and your health hasn’t declined, your income might rise by around 2.5% due to age alone — to roughly £6,968.07, just £169.95 a year more.

At that rate, it would take around 40 years to recoup the single year of income missed by delaying — meaning you’d need to live to 102 just to break even.

The Perfect Storm

Don’t forget that things may not work in your favour at all. If both your fund value and annuity rates were to fall by 5% during the delay, you’d end up with a lower annuity than you could have secured a year earlier. Statistically, you may never recoup this lost income.

The worst thing you could do to your pension pot is nothing at all.

The example used on this page is for illustration purposes only, based on a hypothetical pension fund value, and does not represent a real quote, guaranteed rates, or actual outcomes. Annuity rates and fund values change regularly and depend on your individual circumstances. We will not provide you with advice or recommendations as part of our annuity comparison service — we research the whole of the market and present you with the best available rates, and it is your decision how to proceed.

Retirement Professionals Ltd is an appointed representative of pi financial ltd, authorised and regulated by the Financial Conduct Authority. FCA number 622943.